Economic Overview

Inflation and interest rates remained points of interest across Q1, but towards the end of the quarter attention turned to the consequences of higher interest rates and what they might potentially break. Global growth appeared to be heading in the right direction, as rebounds in various purchasing managers’ indices and business surveys indicated positive sentiment. This was further boosted by China reopening and lower energy prices, however the March collapse of Silicon Valley Bank prompted concerns in the financial space and volatility in the banking sector. Geopolitics remained a factor, with the war in Ukraine ongoing and further tensions between the US and China. While inflation continued to ease across many economies, it remained relatively high in Q1, leaving central banks to tighten monetary policy further. Despite the late quarter sell off, there were positive returns in the major asset classes. The Australian market posted a fair gain, while global equity markets were up strongly for the quarter.

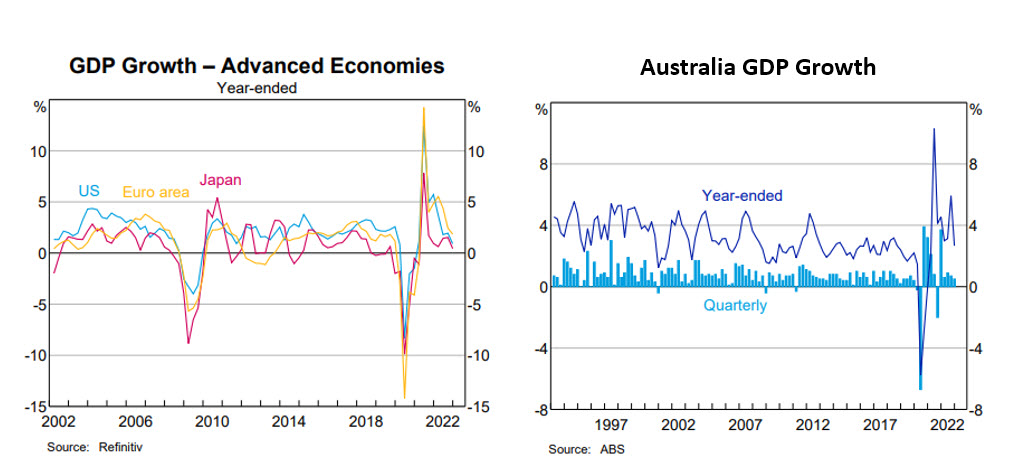

In the US, GDP grew at an annualised rate of 2.6% in Q4 2022, slightly less than initial estimates. Data published since the beginning of 2023 suggests that the US economy continued near that pace in Q1 2023, with real-time GDP tracking indicating 2.5% annualised. February CPI showed headline inflation falling to 6.0% year on year. This was the eighth consecutive monthly decline, down from 8.9% in June. Inflation is now dominated by shelter costs, these now account for over 70% of the increase in the CPI figure. The Federal Reserve raised rates 0.25% twice during Q1. The second increase arrived after the collapse of Silicon Valley Bank, where the Fed expressed confidence in the resilience of the banking system.

The US labour market remains resilient, February non-farm payrolls grew by a stronger-than expected 311,000, while average hourly earnings rose by 4.6% year on year, with unemployment sitting at 3.6%. There have been corporate layoffs in some sectors, notably technology, as companies are taking the opportunity to cut projects and eliminating staff they couldn’t afford to lose previously. Work trends also appear to be reverting to pre covid expectations. According to a Department of Labor survey 72.5% of businesses said their employees rarely or never worked from home in 2022, up from 60.1% in 2021. This means around 21 million more workers were on-site full time in 2022.

Source: RBA 2023

In the Eurozone, the European Central Bank raised interest rates by 0.5% in both February and March. Eurozone inflation was at a one year low in March, sitting at 6.9%, down from 8.5% in February. However, core inflation (excluding food and energy costs) rose to 5.7% from 5.6%. The flash purchasing managers’ index reached a 10-month high of 54.1 in March, although growth was fueled by the service sector with the manufacturing below 50 (above 50 = expansion). A week after the failure of Silicon Valley Bank, troubled Swiss investment bank Credit Suisse was bought by UBS in a deal brokered by the Swiss authorities. While there were some concerns, most quickly accepted Credit Suisse’s problems were contained. In France, plans to raise the retirement age from 62 to 64 saw widespread protests and President Macron’s government narrowly survived a no-confidence vote on the issue.

In the UK, quarterly GDP data showed the UK economy had not contracted in Q4 2022, contrary to expectations. As a result, the economy dodged a technical recession by avoiding two consecutive quarters of decline after Q3’s decline. Energy prices have fallen significantly, as the European energy crisis eased. The Bank of England’s Monetary Policy Committee voted to continue to raising interest rates moving upward by 0.25% in March to 4.25%, while leaving the door open to further tightening, if necessary, but expiring fixed rate mortgages may do some of this work. On the inflation front, headline CPI sat at 10.4%, with core CPI at 6.2% year on year for February. UK inflation proved stronger than expected, due to the resilience of the domestic economy. Composite PMI for March dropped slightly from 53.1 to 52.2, but remains in expansion territory, while consumer confidence continues to surprise to the upside.

In Japan, 2022 GDP growth came in at a modest 1.1% after a 1% contraction in Q3 and a smaller than expected recovery in Q4. Like other economies Japan is still dealing with elevated inflation, albeit at a more modest rate of 4.3%, but this remains high in comparison to recent decades. Attention was still on the surprise December announcement by the Bank of Japan to allow the yields on long-dated government bonds to increase. In January, the BoJ bought $182 billion in bonds to defend their new yield cap. Contrary to expectation, rates were left on hold at the BoJ’s January policy meeting.

In China, US-China tensions resurfaced during the quarter following the shooting down of a Chinese weather (or spy) balloon in US airspace, but there was still optimism about the re-opening of the economy and a potential easing of regulatory pressure on the internet sector. Inflation has remained subdued, allowing the People’s Bank of China to maintain relaxed monetary policy. Excess savings accumulated during lockdown are expected to fuel a recovery via the services sector. This was reflected in the Services PMI reading, which rebounded to 55 in February. Despite strong potential for economic growth, China’s February CPI reading still came in below expectations, increasing only 1% year on year, while the producer price index stayed in deflation territory, falling 1.4%. In response, the PBOC announced a 0.25% cut to its reserve requirement ratio for banks in March.

In Emerging Markets, Brazil saw softening economic data and anti-government riots that damaged government buildings in January. India also saw economic data below consensus expectations. South Africa continues to suffer an ongoing electricity crisis, while it was also ‘grey-listed’ in February by the Financial Action Task Force given its slow progress implementing processes to combat money laundering and terrorist financing.

Back in Australia, data released in March showed GDP increasing by 0.5% for Q4 2022, with the economy growing by 2.7% year on year, showing the economy is still robust. Inflation remained elevated, Monthly CPI came in at 6.8% for the 12 months ending February 2023, down from 7.4% in January. The largest price increases were seen in housing, food, and transport. The savings rate fell to 4.5% in Q4 22, the lowest level since 2017 as interest payments increased. Despite elevated inflation, the RBA continued with 0.25% rate increases at its February and March meetings, noting that it expected inflation to moderate, but services and rent inflation remained high.

Despite the ongoing interest rate increases, some experts were scratching their heads as the housing market, specifically in Sydney appeared to do an abrupt turn during the second half of the quarter. While the national change in dwelling values was down -0.6% across the quarter according to CoreLogic, it was up 0.6% in March. Sydney doing most of the lifting, up 1.4% for the month, albeit still down -12.1% since April 22. Notably, Hobart and Canberra were the only capital markets not to stage any recovery, with Hobart down -12.9% for the year, -4% for the quarter and -0.9% for March. Canberra was down -8.1% for the year, -2% for the quarter and -0.5% for March.

Market Overview

Asset Class Returns

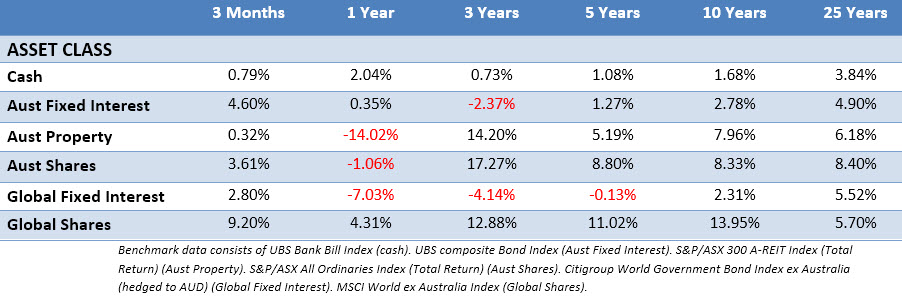

The following outlines the returns across the various asset classes to 31 March 2023.

Global sharemarket returns were strong in Q1, despite the fallout from the failures of Silicon Valley Bank and Credit Suisse. Both failures led to significant volatility in markets towards the end of Q1. The Australian market was more subdued, but still posted a decent return. Australian listed property began to stage a recovery in the first half of the quarter and was up over 10% at one point, but by the end of the quarter had given up most of its gains. Bond prices strengthened across Q1 as yields eased towards the end of the quarter. The 10-Year US Treasury yield started Q1 at 3.88% moving above 4% by end February, but dropped in March with banking concerns, ending the quarter at 3.48%. US 2-year yields also moved higher until March, then slipped back, ending Q1 at 4.06%. In the UK, the 10-year yield fell from 3.67% to 3.49%, while the Australian 10-year yield fell from 4.04% to 3.30%.

In the US, the S&P 500 was up 7.5% for the quarter, albeit down from its January peak, with selloffs in February and early March, before a late quarter rally to recover some earlier gains. The Russell 2000 small-cap index saw the most pain from the banking crisis, due to a higher financial sector weighting. While the Russell 2000 finished up 2.75% in Q1, it was up almost 14% at the beginning of February. Despite the banking and financial sector issues, the energy and healthcare sectors struggled the most over the quarter, while communication services and the technology sectors were both up more than 20%.

The Silicon Valley Bank (SVB) failure was the most notable issue in the US during the quarter. While there were concerns about contagion, SVB was more of an isolated issue with a narrow customer base and poor risk management. SVB took large deposits from start-up tech companies and used these deposits to purchase longer term debt. The sharp increase in interest rates over the past year meant the value of these assets declined significantly. With the tech sector under stress, many depositors began to withdraw their funds. SVB was forced to sell some of its long-term debt at a significant loss, and word began to spread, resulting in a bank run. Because many of its customers had abnormally large deposits, above the government insurance mark of $250k, it explains the panic, although the US administration later said it would honour all deposits.

Eurozone shares were the best performer of the major regions despite banking sector volatility, with the French and German markets posting double digit gains. One of Europe’s biggest concerns over the past year was energy security due to the Russian invasion of Ukraine, but a very mild winter and a significant emphasis on finding new sources of natural gas has helped restore confidence. Technology, consumer discretionary and communication services sectors were the strongest performers, while real estate struggled due to higher financing costs and weaker occupancy rates. Despite the troubles with Credit Suisse, the eurozone financials sector still managed gains for the quarter as the problem was viewed as being quickly contained.

UK shares posted modest gains over Q1, with strong moves across January and February, but global banking concerns saw the UK market sell off sharply in early March, without the late March recovery rally seen in other markets. Economically sensitive areas, such as consumer discretionary, outperformed in line with other markets. This reflected a strong recovery in domestically focused areas and hopes central banks may be able to cut interest rates in late 2023. As with other markets, real estate was the worst performing sector. Large companies held up, with smaller companies losing ground.

In Japan, shares rose strongly in Q1 with the Nikkei index up 9%. Quarterly earnings results announced across the late January to mid February period were mixed. Exporters had a difficult time due to yen appreciation during Q4 2022, while a slowdown in production mainly affecting the technology sector. Domestic focused companies recorded better than expected sales numbers, but suffered from cost increases. The Silicon Valley Bank collapse and the bailout of Credit Suisse by UBS dragged the market lower, with Japanese financial stocks hit hard, but the broader market almost recovered by the end of the quarter.

Asia (ex-Japan) and Emerging markets were positive across Q1 with the new year bringing renewed optimism about the re-opening of China’s economy. Chinese shares saw robust gains in January, but were mostly flat for the rest of Q1. The strongest gains came from Taiwan, Singapore, the Czech Republic and Mexico. India saw negative returns, as Adani Group was hit with allegations of fraud and share price manipulation early in the quarter, investors also soured on India as economic growth stalled. While emerging markets posted positive returns over the quarter, the broader index still lagged the developed market MSCI World Index.

The Australian market (All Ords Accumulation) was up 3.61% in Q1 and strongly in January, but relinquished most of those early gains as concerns around banking grabbed attention in March. As in many other developed markets, consumer discretionary was the best performing sector, up over 10%, followed by communication services and consumer staples. In fact, most sectors posted healthy gains, higher than the index itself, with the only negative sectors in Q1 being energy and financials. Financials were down -2.69%, with their heavy weighting being the biggest drag on ASX performance for the quarter.

Remembering Dan Wheeler

During the quarter, Dan Wheeler, a financial advice industry pioneer passed away. Wheeler had a large influence on changing the financial advice industry for the better, not just in his native US, but across the world. The things that Dan did had an an influence on us and our colleagues. There were many obituaries written and the UK Financial Times picks up Dan’s early life:

Wheeler grew up in a working-class neighbourhood in East St Louis, where his mother was a nurse and his father an accountant. He drifted into studying history at a small liberal arts college before volunteering for the Marine Corps in the middle of the Vietnam war — a typically jarring change.

After returning from Vietnam, Dan bounced between jobs before being offered a position as a stockbroker.

Merrill’s brokers seemed clueless. Wheeler thought they basically just ripped off clients by churning money to generate trading commissions. But then he discovered the works of Gene Fama, the University of Chicago professor and father of the efficient markets hypothesis. It all suddenly makes sense, Wheeler thought.

As a present to himself on his 40th birthday, Wheeler quit Merrill to be an independent financial adviser. Rather than being paid through commissions, he chose a “fee only” model. That meant Wheeler for the most part bunged his clients’ money into the Vanguard 500 index fund, one of the few cheap passive funds broadly available to ordinary American investors at the time.

Later Dan founded the financial advice services side of investment manager Dimensional Fund Advisors. Over his career Dan coached many dispirited advisers who’d only been trained to see clients as a dollar sign or to push high-cost funds on them, this from our US colleague Jeff Troutner:

I met Dan at a low point in my career. I had already escaped from the sales side of the industry as a stockbroker. I then joined a market timing firm that failed me and my clients after two years. And, finally, my attempt to build an advisor profile service failed after I realized most advisors were misrepresenting their performance and I couldn’t be part of their lie.

Three strikes. I was well on my way out of the investment business.

But as fate would have it, Dan understood where my head was and took the time to share with me his personal story. His journey in the industry was so similar to my own—and the alternative he suggested was so compelling—that I was immediately filled with new optimism and ambition.

I honestly didn’t think people like Dan existed in the investment industry. He gave me another chance at the plate and showed me how to hit a home run: eliminate conflicts of interest, don’t pick stocks and time markets, and report client performance clearly and accurately at all times. Let markets work. Be patient. Be strong for clients.

From US adviser Eric Nelson:

One story I remember Dan telling sticks with me to this day. A large new client, recently divorced, came to him to invest her money. Her life was not in good shape; she was drinking too much and not in a place where she could make the best long-term financial decisions. Dan could have invested the money and earned an advisory fee, but instead, he told the client that she needed to work on herself, go to alcohol rehabilitation, and when she got clean, he would be there to help her take positive steps forward. In the meantime, Dan put the account in T-bills and never charged her for his time and advice. That’s a bold thing to tell someone, but when you care about them, you stick your neck out like that. There is a saying that “people don’t have money problems; money has people problems.” That’s what personal financial advising is about, and what you need to appreciate to truly help people with their money. Dan never failed to remind us of that simple fact.

Vale Dan Wheeler.

This material is provided for information only. No account has been taken of the objectives, financial situation or needs of any particular person or entity. Accordingly, to the extent that this material may constitute general financial product advice, investors should, before acting on the advice, consider the appropriateness of the advice, having regard to the investor’s objectives, financial situation and needs. Are you looking for a Canberra financial adviser? This is not an offer or recommendation to buy or sell securities or other financial products, nor a solicitation for deposits or other business, whether directly or indirectly.